Tax incentives

If you conduct business in depopulated areas or areas where peninsula revitalization measures are being implemented, you may be eligible for tax benefits based on various laws.

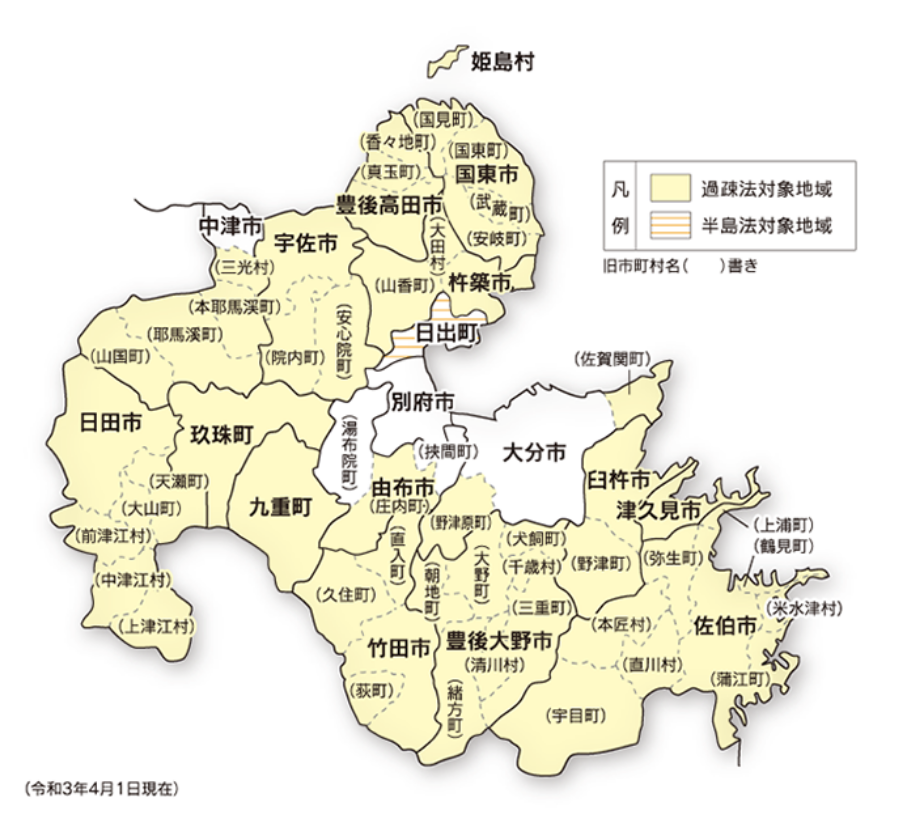

Special Measures Act on Support for Sustainable Development in Depopulated Areas (Depopulation Act) Act No. 19 of March 31, 2021

Designated municipalities

Bungotakada City, Usa City, Kunisaki City, Himeshima Village, Kitsuki City, Taki City, Tsukumi City, Oita City (former Nozuhara Town, former Saganoseki Town), Yufu City (former Shonai Town), Saiki City, Taketa City, Bungo-Ono City, Kokonoe Town, Kuju Town, Hita City, Nakatsu City (former Sanko Village, former Honyamakei Town, former Yamakuni Town)

* Only the areas within the brackets are included in the municipalities listed in parentheses.

Tax

| Eligible criteria | Tax reduction details | |||||

|---|---|---|---|---|---|---|

| Target Audience | Target industries | Acquisition price requirements ※3※4 | ||||

| A corporation or individual filing a blue return who acquires, produces, or constructs the following facilities: *1 |

Manufacturing and Hotel Industry |

Building auxiliary facilities *2 Machinery and equipment structures |

・Capital of 50 million yen or less → Total of 5 million yen or more *5 ・Capital of 50 million yen to 100 million yen or less → Total of 10 million yen or more *5 ・Capital of over 100 million yen → Total of 20 million yen or more |

National Tax | Corporate tax (income tax) | Extra depreciation (5 years) Machinery and equipment 32/100 Buildings 48/100 |

| Local taxes | Business tax※6 | Tax exemption (3 years) | ||||

| Real estate acquisition tax※7 | Tax exemption | |||||

| Sales of agricultural, forestry and fishery products, information services, etc. |

Total of 5 million yen or more*5 | Property tax*8 | Tax exemption (3 years) | |||

*1 Businesses with capital exceeding 50 million yen are only eligible for acquisition through new construction or expansion.

*2 Facilities attached to buildings are only eligible when acquired together with the building.

*3 For corporations with a consolidated parent corporation for tax purposes, the capital of the parent corporation is used for the determination.

*4 If accelerated depreciation has been applied through subsidies, etc., the value after the accelerated depreciation is used for the determination.

*5 The total amount of fixed assets (limited to those directly used for business purposes) acquired per business year is determined.

*6 Calculated by "income that should be the tax base in Oita Prefecture x number of employees related to the newly constructed or other facilities / number of employees in the prefecture".

*7 Tax exemption for land is only available if construction of the house begins within one year from the day after the acquisition date.

*8 Only the portion directly used for business purposes is eligible for tax exemption.

Peninsula Development Act June 14, 1985, Act No. 63

Designated municipalities

Hiji Town

Tax

| Eligible criteria | Tax reduction details | |||||

|---|---|---|---|---|---|---|

| Target Audience | Target industries | Acquisition price requirements | ||||

| A corporation or individual that files a blue return and acquires, produces, or constructs the following equipment: | Manufacturing and Hotel Industry |

Building auxiliary equipment and machinery structures |

・Capital of 10 million yen or less → Total of 5 million yen or more ・Capital of 10 million yen to 50 million yen or less → Total of 10 million yen or more ・Capital of 50 million yen or more → Total of 20 million yen or more |

National Tax | Corporate tax (income tax) | Extra depreciation (5 years) Machinery and equipment 32/100 Buildings 48/100 |

| Local taxes | Business tax*1 | First year: 1/2 tax 2nd year:3/4 tax 3rd year:7/8 tax |

||||

| Real estate acquisition tax*2 | 1/10 tax | |||||

| Sales of agricultural, forestry and fishery products, information services, etc. |

Total of 5 million yen or more | Property tax*3 | First year: 1/10 taxation Second year: 1/4 taxation Third year: 1/2 taxation |

|||

Areas subject to the Depopulation Act and the Peninsula Act

*1 Calculated by: "Income that should be the tax base in Oita Prefecture x number of employees related to the newly installed equipment / number of employees in the prefecture".

*2 Land tax exemption is only available if construction of a house begins within one year from the day after the acquisition date.

*3 Only the portion directly used for business purposes is eligible for tax exemption.

Remote Islands Development Act

When making capital investments on remote islands, tax benefits are available if certain requirements regarding industry and acquisition price are met.

Target area

Himeshima Village, Tsukumi City (Mukushima Island, Hodo Island), Saiki City (Oinu Island, Oshima Island, Yakatajima Island, Fukashima Island)

For details, please contact the Kumamoto Regional Taxation Bureau or your nearest tax office for national taxes, the Prefectural General Affairs Department Taxation Division (097-506-2384) or

your nearest prefectural tax office for business taxes and real estate income taxes, and the relevant city, town, or village office for property taxes.

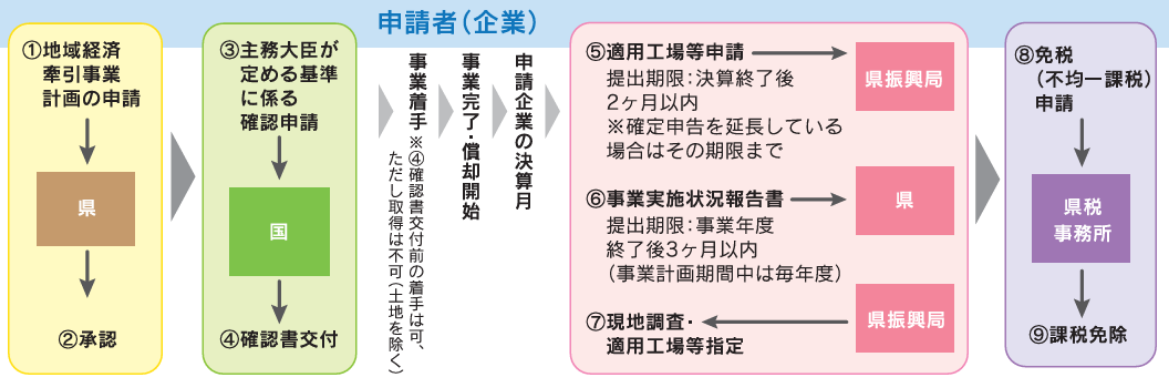

Regional Future Investment Promotion Act

If you submit a "Regional Economic Leading Business Plan" to the prefecture during the planning stage (before construction begins) and it is approved, you will be eligible for the following various preferential treatment measures.

Requirements for approval of regional economic driving business plans (Prefectures)

(1) The target industry is one of the following, and the added value (※1) increases by 46 million yen or more (※2)

| Target Industries | ①Automobile-related industries ②Electronics, electrical and machinery-related industries ③Material-based industries and shipbuilding-related industries ④Medical equipment-related industries ⑤Environmental and energy-related industries ➅Food, agriculture, forestry and fisheries-related industries (only if the prefecture's specialty products are utilized) ⑦Service industries (only if the prefecture's tourism resources are utilized) ⑧Digital-related industries ⑨Aerospace-related industries ⑩Logistics-related industries |

|---|

*1 Added value = Sales revenue – Total expenses (cost of sales + selling, general and administrative expenses) + Total wages + Taxes

(2) Satisfy any of the following (determined by business establishments within the prefecture) (※3):

1) The amount of transactions between businesses within the prefecture has increased by 15 million yen since the start of the program ;

2) Sales have increased by 330 million yen since the start of the program ;

3) The number of employees has increased by 10 people since the start of the program;

4) The amount of wages, etc. paid has increased by 30 million yen since the start of the program.

(※2) (※3) Values assuming a business plan period of 5 years. If the plan period is shorter than that, the value is calculated by dividing the plan period by 5 years.

Overview of preferential treatment

Special tax treatment for local taxes (real estate acquisition tax, fixed asset tax)

You will need to apply for certification from the government and receive a certificate of certification.

Requirements

All of (1) to (4) must be met. *For detailed requirements, please check the Oita Prefecture website.

(1) Investment amount requirement (for items acquired by March 31, 2028)

| Industry | Amount | Other necessary information | |

|---|---|---|---|

| Target assets | Acquisition price | ||

| Agriculture, forestry and fisheries | Land, buildings, attached facilities and structures | Over 50 million yen | 25% or more of the depreciation expenses for the previous fiscal year * *If the target business is a consolidated company, the depreciation expenses for all other companies included in the same consolidated scope are to be added together |

| Other industries | Land, buildings, attached facilities and structures | Over 100 million yen | |

(2) Sales growth rate must increase to a certain level.

(3) Other (return on investment, labor productivity, etc. must be met.)

(4) The company must be a corporation that files a blue tax return.

nefits

| Real estate acquisition tax | Tax exemption |

|---|---|

| Property tax | Tax exemption (for the first three years), etc. |

・Assets eligible for tax exemption = land, buildings, attached facilities, and structures

pecial provisions for corporate tax

You need to apply for certification from the government and receive a certificate of certification.

Requirements

(1) "Investment amount ≧ 100 million yen" and "Investment amount ≧ 25% of the previous year's depreciation expense" (for assets acquired by March 31, 2028)

(2) to (4) are the same as the "Special tax treatment for local taxes (real estate acquisition tax, fixed asset tax)"

Benefits

| Target equipment | Special depreciation | Tax Credit |

|---|---|---|

| Machinery and equipment | 35% | 4% |

| If the additional requirement *4 is met | 50% | 5% |

| If you meet the medium-sized enterprise quota*5 | 50% | 6% |

| Buildings, facilities and structures | 20% | 2% |

*4

- The increase in added value in the most recent fiscal year is 8% or more.

- The average added value for the most recent two fiscal years is 5 billion yen or more, and the added value is generated by 300 million yen or more

- The business is in an industry that contributes to the growth and development of the local economy, and the capital investment is 1 billion yen or more.

- Meet any of the above 1 to 3, and the growth rate of labor productivity and return on investment are 5% or more, and the added value generated is 100 million yen or more

*5

- A specific medium-sized enterprise as defined by the Industrial Competitiveness Enhancement Act, and has been confirmed as having management capabilities

- The capital investment is 1 billion yen or more, and a partnership construction declaration has been registered

- Meet requirements 1 and 2 of *4, and the growth rate of labor productivity and return on investment are 5% or more

- The investment limit for this scheme is 8 billion yen.

- If special depreciation expenses are not recorded up to the limit, the depreciation shortfall can be carried over to the following fiscal year.

- The tax credit is capped at 20% of the corporate tax amount for the fiscal year in question.

- This scheme does not support the use of eligible assets for loan purposes or the acquisition of used assets.

others

(1) Reduction in interest rates on equipment loans by the Japan Finance Corporation

(2) Separation of guarantees by credit guarantee corporations

(3) Debt guarantees by the Food Distribution Structure Improvement Promotion Organization

(4) Reduction in patent fees (limited to small and medium-sized enterprises) and reduction in registration fees for regional collective trademarks

For more information, please contact each organization.

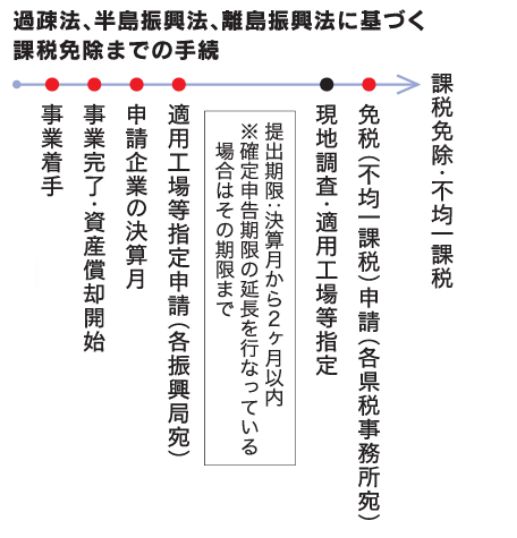

Procedures for tax exemption under the Regional Future Investment Promotion Act

Comparison of preferential treatment in the Depopulation Law and the Regional Future Investment Promotion Law

Special Measures Act for the Sustainable Development of Depopulated Areas

Applicability requirements

| Target industries | Target area | Target assets | Acquisition price | others | ||

|---|---|---|---|---|---|---|

| National Tax | Local taxes | National Tax | Local taxes | |||

| Manufacturing industry, hotel industry, agricultural, forestry and fishery product sales industry, information service industry, etc. |

gnated municipalities | Building auxiliary facilities, structures, machinery and equipment |

Varies depending on industry and capital | ― | ||

Benefits

| Taxation | others | ||||

|---|---|---|---|---|---|

| National Tax | Local taxes | ||||

| Extra depreciation | Tax Credit | Business Tax | Real estate acquisition tax | Property tax | |

| 〇(5 years) | ― | 〇 (3 years) | 〇 | 〇(3年間) | ― |

Application deadline

March 31, 2027

Pre-application procedures

Not required

Regional Future Investment Promotion Act

Applicability requirements

Target industries |

Target area | Target assets | Acquisition price | others | ||

|---|---|---|---|---|---|---|

| National Tax | Local taxes | National Tax | Local taxes | |||

| 10 industries stipulated in the prefecture's basic plan | All areas | Depreciable assets | Land, buildings, attached facilities and structures | Over 100 million yen | Over 100 million yen | The business is innovative. |

Benefits

| Taxation | others | ||||

|---|---|---|---|---|---|

| National Tax | Local taxes | ||||

| Extra depreciation | Tax Credit | Business Tax | Real estate acquisition tax | Property tax | |

| 〇 | 〇 | ― | 〇 | 〇 (3 years) | Low-interest loans, etc. |

Application deadline

March 31, 2028

Pre-application procedures

Required

Small and Medium Enterprise Management Strengthening Law (Small and Medium Enterprise Management Strengthening Tax System)

Eligible persons: Small and medium-sized enterprises filing blue tax returns who will install the applicable equipment by the end of March 2025

Incentives

Immediate depreciation or tax deduction of corporate tax etc. on acquired assets

Eligible items: Building accessories, machinery, tools, fixtures, and software.

Acquisition price requirements: Must be above a certain price.

Machinery: 1.6 million yen. Tools and fixtures: 300,000 yen.

Building accessories: 600,000 yen. Software: 700,000 yen.

Other requirements :

- It must be production facilities (facilities directly used for business purposes)

*Office equipment and fixtures, building and auxiliary facilities related to head offices, etc. are not eligible. - It must be a domestic investment.

- It cannot be a used asset or a rental asset, etc.

Introduction of equipment to improve productivity

- Target equipment

- Single equipment

- Necessary procedures

- Please obtain a certificate from the equipment manufacturer.

- Requirements

- Equipment with an average annual productivity improvement of 1% or more compared to the previous model

Introducing equipment to improve profitability or digitalize equipment

- Target equipment

- Multiple equipment allowed

- Necessary procedures

- Prepare an investment plan and have it reviewed in advance by a certified public accountant or tax accountant.

- Requirements

- For profit-enhancing equipment, the average annual return on investment must be 5% or more.

- Digitalization equipment: Equipment that enables remote operation, visualization, or automated control.

*1 When introducing any of these types of equipment, it is necessary to set up a management evolution methodology for small and medium-sized enterprises, etc.

Contact

- Contact name

- Ministry of Economy, Trade and Industry, Kyushu Bureau of Economy, Trade and Industry, Management Support Division

- TEL

- 092-482-5593

Regional Revitalization Act (Regional Base Strengthening Tax System)

When relocating or expanding head office functions, you can apply for a "Plan for the Development of Specific Business Facilities in Regional Vitality Improvement Areas, etc." at the planning stage (before construction begins) and receive preferential treatment such as tax exemptions and debt guarantees by receiving approval.

Target Audience

| Relocation type | Expanded type |

|---|---|

| Businesses that are relocating their head office functions from Tokyo's 23 wards to Oita Prefecture |

|

Scope of head office functions (special business facilities)

Business location

Those who carry out business across multiple business locations or company-wide business

Research and Planning Division

A department that develops standards and plans for businesses and products, and conducts market research

Information Processing Department

Departments that specialize in developing systems and programs for their own company (not for commercial purposes) Departments that conduct basic research, applied research, and development research

Research and Development Department

Departments conducting basic research, applied research, and development research

International Business Division

A department that handles trade operations related to imports and exports and oversees overseas business.

Other Management Department

A department that handles general affairs, accounting, and human resources management.

Information Services Business Division

A division that develops software, provides information processing and provision services, and provides Internet-related services.

Part of the Commercial Business Division

A department that handles sales and purchasing operations that are conducted exclusively within the company using telephone and online tools.

Part of the Service Business Division

A department that handles research and planning, information processing, research and development, international business, and other management-related outsourcing.

Research Institute

Those who play an important role in research and development by business operators (including research and development facilities within factories)

Training Center

Playing an important role in human resource development by business operators

Requirements for certification of plans

- It must conform to the Oita Prefecture Certified Regional Revitalization Plan (Oita Prefecture Regional Vitality Improvement Area Specific Business Facility Development Promotion Project)

- The number of full-time employees at the specific business facility must increase by 5 people (1 small and medium-sized business owner) or more

(in the case of relocation, the majority of employees must be transferees from businesses in the 23 wards of Tokyo within one year from the date the specific business facility is put into use for business purposes, and thereafter, the number must be 1/4 or more during the plan period)

Note: Permanent employment refers to employment in which the scheduled working hours per week are 20 hours or more and the employment period is not set or is renewed repeatedly.

Overview of preferential treatment

When relocating or expanding head office functions, you can apply for a "Plan for the Development of Specific Business Facilities in Regional Vitality Improvement Areas, etc." to the prefecture at the planning stage (before work begins) and receive preferential treatment such as tax exemptions and debt guarantees by receiving approval.

Special local tax treatment (plans must be approved by March 31, 2026)

Eligible: Depreciable assets used for business purposes such as land and specific business facilities

Acquisition price requirements: Total amount must be 38 million yen or more (SMEs, etc.: 19 million yen)

| Relocation type | Expanded type | |

|---|---|---|

| Corporate business tax | Tax exemption (3 years) | ― |

| Real estate acquisition tax | Tax exemption | 1/10 tax |

| Property tax | Tax exemption (for 3 years), etc. | 1st year: 1/10, 2nd year: 1/3, 3rd year: 2/3 tax, etc. |

- Those who have been in service for three years since the day following the date of plan approval are eligible

- The tax rate for non-uniform fixed asset tax may differ depending on the city, town, or village.

Special provisions for corporate tax (plans must be approved by March 31, 2026)

[Office tax reduction] Special depreciation or tax deduction for corporate taxes etc. on acquired assets

Eligible: Buildings, attached facilities, and structures

Acquisition price requirements: Total amount must be 35 million yen or more (Small and medium-sized enterprises, etc.: 10 million yen)

| Relocation type | Expanded type |

|---|---|

| Special depreciation 25% or tax credit 7% | Special depreciation 15% or tax credit 4% |

Limit: Tax credit is 20% of the current corporate tax amount

- Only parts related to head office functions are applicable. (Calculated by dividing the floor area)

- Those that have been in service within three years since the day following the date of plan certification are applicable.

- If a subsidiary company has entered an office acquired by a parent company and is used for business purposes, it is not applicable.

- Only those that have never been used for business purposes are applicable.

[Employment Promotion Tax System] Tax deductions for corporate taxes etc. related to increased employee numbers

Requirements: There are no employees who left the company due to employer reasons during the applicable fiscal year, the fiscal year before that, or the fiscal year before that.

| Relocation type | Expanded type |

|---|---|

| First year: Maximum 900,000 yen/person (500,000 yen + additional 400,000 yen) Three-year total: Maximum 1,700,000 yen/person |

First year only: 300,000 yen/person |

|

|

Limit: 20% of the current corporate tax amount

*Office tax reduction and employment promotion tax system cannot be used together in the same fiscal year (office tax reduction and employment promotion tax system top-up can be used together).

| Low-interest loans from the Japan Finance Corporation | Debt guarantee by the Organization for Small & Medium Enterprises and Regional Innovation |

|---|---|

| Equipment financing for SME business: Special interest rate up to 270 million yen③ (Standard interest rate for other working capital, etc.) For details, please contact the Japan Finance Corporation Head Office (Small and Medium Enterprise Business) that has jurisdiction over your head office . |

Issuance of corporate bonds, debt guarantees for corporate bond issuance and borrowing from financial institutions .

|